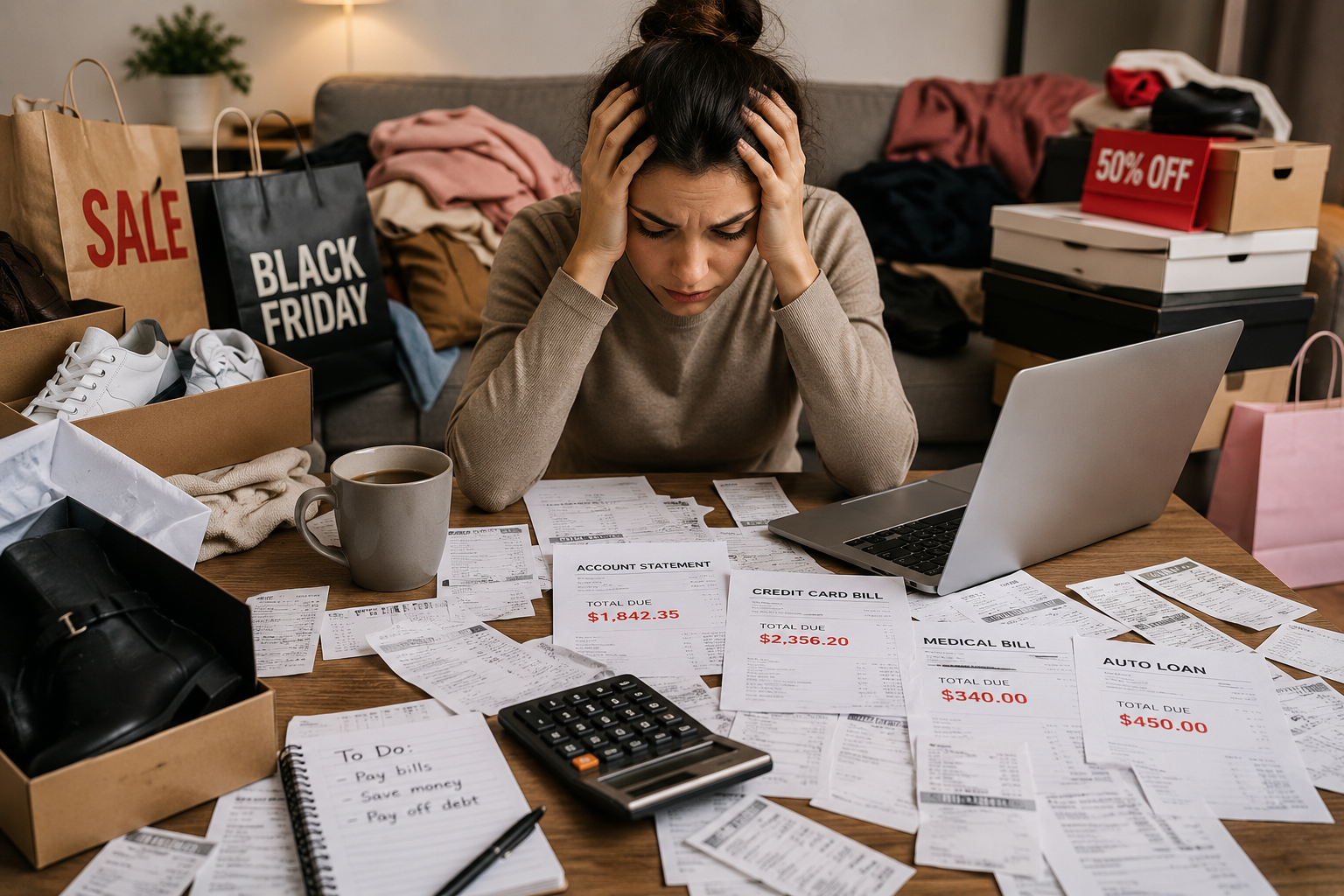

Many people work hard to improve their finances, save money, and achieve long-term goals. However, one habit often stands in the way of financial progress: impulse buying. Small unplanned purchases may seem harmless at first, but over time they can create serious financial problems and delay important goals.

Impulse buying is more common than many people realize. Whether it is online shopping, flash sales, or buying items simply because they look appealing, impulsive spending can slowly damage your budget and reduce your ability to save money.

Understanding how impulse buying affects your finances is the first step toward building healthier spending habits and achieving greater financial stability.

What Is Impulse Buying?

Impulse buying happens when someone makes an unplanned purchase without carefully considering whether the item is necessary or affordable.

These purchases are usually driven by emotions rather than logic. People may buy something because they feel excited, stressed, bored, or influenced by advertising.

Examples of impulse buying include:

- Purchasing clothes you did not plan to buy

- Adding unnecessary items to your online shopping cart

- Buying expensive gadgets without researching them

- Spending money during sales simply because prices seem lower

- Ordering food frequently without budgeting for it

While occasional spontaneous purchases are normal, repeated impulse buying can seriously affect financial health.

Why People Make Impulse Purchases

Understanding the causes of impulse buying can help people make better financial decisions.

Emotional Spending

Many people shop when they feel emotional. Stress, sadness, anxiety, or even happiness can trigger unnecessary spending.

Shopping sometimes provides temporary excitement or comfort, but the emotional satisfaction usually fades quickly.

Advertising and Marketing

Companies spend billions on advertising designed to encourage impulse purchases. Limited-time offers, discounts, and targeted online ads create urgency and temptation.

Phrases like “buy now,” “limited stock,” or “today only” are designed to encourage quick decisions.

Social Pressure

Social media often encourages people to compare themselves to others. Seeing influencers or friends showing expensive products can create pressure to spend money unnecessarily.

Easy Online Shopping

Online shopping has made impulse buying easier than ever. With saved payment information and one-click purchases, people can buy items within seconds.

Lack of Financial Planning

Without a clear budget or financial goals, people may spend money without understanding how their choices affect their future.

How Impulse Buying Damages Financial Goals

Impulse buying may seem small in the moment, but repeated spending can create major long-term consequences.

Reduces Your Ability to Save Money

Every unnecessary purchase reduces the amount of money available for savings.

For example, spending an extra $10 or $20 several times each week can add up to hundreds or even thousands of dollars each year.

That money could instead be used for:

- Emergency funds

- Retirement savings

- Paying off debt

- Travel goals

- Education expenses

- Home purchases

Small daily spending habits often have a larger financial impact than people expect.

Creates Credit Card Debt

Many impulse purchases are made using credit cards. When people buy items they cannot afford immediately, debt begins to grow.

High-interest credit card balances can become difficult to repay, especially when impulsive spending continues regularly.

Debt creates additional financial pressure and reduces future financial freedom.

Delays Important Life Goals

Impulse buying can delay major goals such as:

- Buying a home

- Starting a business

- Building investments

- Becoming debt-free

- Saving for retirement

Money spent on unnecessary purchases cannot be used for long-term financial growth.

Over time, these delays can create frustration and regret.

Increases Financial Stress

Financial stress affects many aspects of life, including relationships, sleep, and mental health.

People who frequently make impulse purchases may later feel guilt or anxiety about their spending habits.

Repeated financial mistakes can also damage confidence and make budgeting feel overwhelming.

Encourages Poor Money Habits

Impulse buying often becomes a habit. The more frequently people make emotional or unplanned purchases, the harder it becomes to control spending.

Healthy financial habits require discipline, planning, and awareness.

The Hidden Cost of Small Purchases

Many people underestimate how much small purchases affect their finances over time.

For example:

- A daily $5 coffee equals about $150 per month

- Frequent online purchases may total hundreds monthly

- Weekly impulse spending can easily exceed several thousand dollars per year

While occasional treats are completely normal, constant unnecessary spending can quietly damage financial progress.

Signs You May Be Struggling With Impulse Buying

Some common signs include:

- Buying items you rarely use

- Shopping when emotional

- Feeling regret after purchases

- Frequently exceeding your budget

- Struggling to save money

- Hiding purchases from family members

- Making purchases simply because items are on sale

Recognizing these behaviors is an important step toward improvement.

How to Control Impulse Buying

Fortunately, impulse buying can be reduced with better financial habits and self-awareness.

Create a Clear Budget

A budget helps you understand exactly where your money is going each month.

When people plan their spending carefully, they are less likely to make unnecessary purchases.

A good budget should include:

- Essential expenses

- Savings goals

- Debt payments

- Reasonable personal spending

Having financial structure improves decision-making.

Use the 24-Hour Rule

Before making non-essential purchases, wait at least 24 hours.

This simple strategy allows emotions to calm down and gives you time to decide whether you truly need the item.

In many cases, the desire to buy disappears after waiting.

Avoid Shopping When Emotional

Stress and emotional situations often lead to poor financial decisions.

Instead of shopping, try healthier alternatives such as:

- Exercising

- Reading

- Spending time with family

- Going for a walk

- Listening to music

Developing non-financial coping habits can reduce emotional spending.

Remove Shopping Temptations

Reducing exposure to marketing can help control spending urges.

Some practical ideas include:

- Unsubscribe from promotional emails

- Delete shopping apps

- Avoid browsing online stores for entertainment

- Limit social media exposure if it triggers spending

Fewer temptations make impulse control easier.

Track Every Expense

Tracking purchases increases awareness of spending habits.

Many people are surprised when they see how much money goes toward unnecessary purchases each month.

Expense tracking can help identify patterns and improve financial discipline.

Set Meaningful Financial Goals

Clear goals make it easier to resist unnecessary spending.

Examples include:

- Building an emergency fund

- Paying off debt

- Saving for travel

- Buying a car

- Investing for retirement

When people focus on long-term rewards, short-term temptations become easier to avoid.

Learn the Difference Between Wants and Needs

One of the most important financial skills is understanding the difference between necessary expenses and optional spending.

Needs include:

- Housing

- Food

- Utilities

- Transportation

- Healthcare

Wants include:

- Luxury items

- Trendy gadgets

- Expensive entertainment

- Unplanned shopping

This awareness improves financial decision-making over time.

Why Delayed Gratification Matters

Successful money management often requires delayed gratification.

Delayed gratification means choosing future benefits over immediate pleasure.

For example:

- Saving instead of overspending

- Investing instead of buying unnecessary items

- Paying off debt instead of financing luxuries

People who practice delayed gratification often achieve stronger long-term financial stability.

Building Better Spending Habits

Improving spending habits takes time and consistency.

Some useful habits include:

- Shopping with a list

- Comparing prices before buying

- Planning purchases in advance

- Using cash for discretionary spending

- Reviewing financial goals regularly

Small behavioral changes can lead to major financial improvements over time.

The Emotional Benefits of Financial Control

Controlling impulse buying does not mean eliminating all enjoyment from life.

Instead, it creates a healthier relationship with money.

People who manage spending wisely often experience:

- Less financial stress

- Greater confidence

- Better savings habits

- More freedom in the future

- Improved financial security

Financial discipline supports both short-term stability and long-term success.

Making Smarter Financial Decisions Every Day

Every spending decision affects your financial future in some way.

Impulse buying may provide temporary excitement, but thoughtful spending creates lasting financial benefits.

Learning to pause before purchasing, follow a budget, and focus on meaningful goals can completely transform your financial life.

Over time, these habits help build greater stability, stronger savings, and a more secure future.

Choosing Long-Term Financial Success

Impulse buying is one of the most common obstacles to financial progress. While occasional spontaneous purchases are normal, repeated emotional spending can lead to debt, stress, and delayed goals.

The good news is that better financial habits can be learned by anyone.

By understanding your spending triggers, creating a budget, and focusing on long-term priorities, you can take control of your finances and make smarter decisions every day.

Small changes today can lead to significant financial improvement in the future.